Portland Office Submarkets

A practical guide to Portland's office districts — what each market offers, how lease economics differ, and how to choose.

Portland's office market is not one market — it's a collection of districts with different building stock, tenant profiles, lease structures, and pricing dynamics. Downtown commands different economics than the 217 Corridor. The Pearl District attracts a different tenant than Kruse Way. And sublease availability, parking ratios, and building class create real functional differences between submarkets that don't show up in headline vacancy rates.

This page provides a fast overview of the key Portland office submarkets and what typically fits where, then links to deeper guides for each area. Coverage spans the Portland metro — CBD, close-in neighborhoods, suburban corridors, and Southwest Washington.

SUBMARKETS

Downtown/CBD

Portland's largest and deepest office market with Class A and B towers concentrated along the transit mall. Building stock ranges from renovated historic product to institutional high-rises. Transit access is the strongest in the metro. Vacancy has created tenant leverage on concessions and TI, but flight to quality means the best buildings still perform differently than commodity product.

Best for: law, finance, accounting, government, and professional services firms prioritizing transit access, institutional presence, and central visibility.

Lloyd District

East-side office market with larger institutional floorplates and proximity to I-84, the Convention Center, and MAX. Lloyd offers a price alternative to CBD with better parking and reasonable transit access. The submarket has absorbed tenant migration from Downtown as companies look for value positioning without losing accessibility.

Best for: mid-size to large professional services, healthcare administration, and tenants seeking CBD-adjacent economics with better parking.

Johns Landing & SW Close-In

Mix of newer Class A construction along the South Waterfront (OHSU, aerial tram, streetcar access) and smaller-scale Class B product along Macadam and the Barbur/Capitol Hwy corridors. South Waterfront inventory is limited and skews toward healthcare and institutional tenants. Johns Landing and the broader SW corridor offer smaller lease sizes, moderate pricing, and a quieter environment — parking and building condition vary significantly between properties.

Best for: healthcare, biotech, and OHSU-affiliated firms on the waterfront side; small professional firms, consultancies, and service businesses seeking close-in location and moderate pricing along the SW corridors.

Explore More →

NW Close-In

Creative and tech-oriented office in converted warehouse and loft buildings mixed with newer construction. Smaller floorplates, exposed structure, and street-level retail access. Parking is limited and typically priced separately. Lease structures vary more than in other districts — building systems in converted product can be older, so operating expense exposure should be evaluated carefully.

Best for: tech, creative, design, marketing, and smaller professional firms that value neighborhood character and walkability over floor size and parking.

Central Eastside & Close-in SE

Emerging office submarket in a historically industrial area transitioning to mixed-use. Building stock includes converted warehouse space, creative office, and newer ground-up construction. Parking is constrained. Zoning and use can be complex — some buildings carry industrial overlay restrictions.

Best for: tech, creative, startups, and firms that value inner Portland proximity and non-corporate environments over institutional amenities and parking.

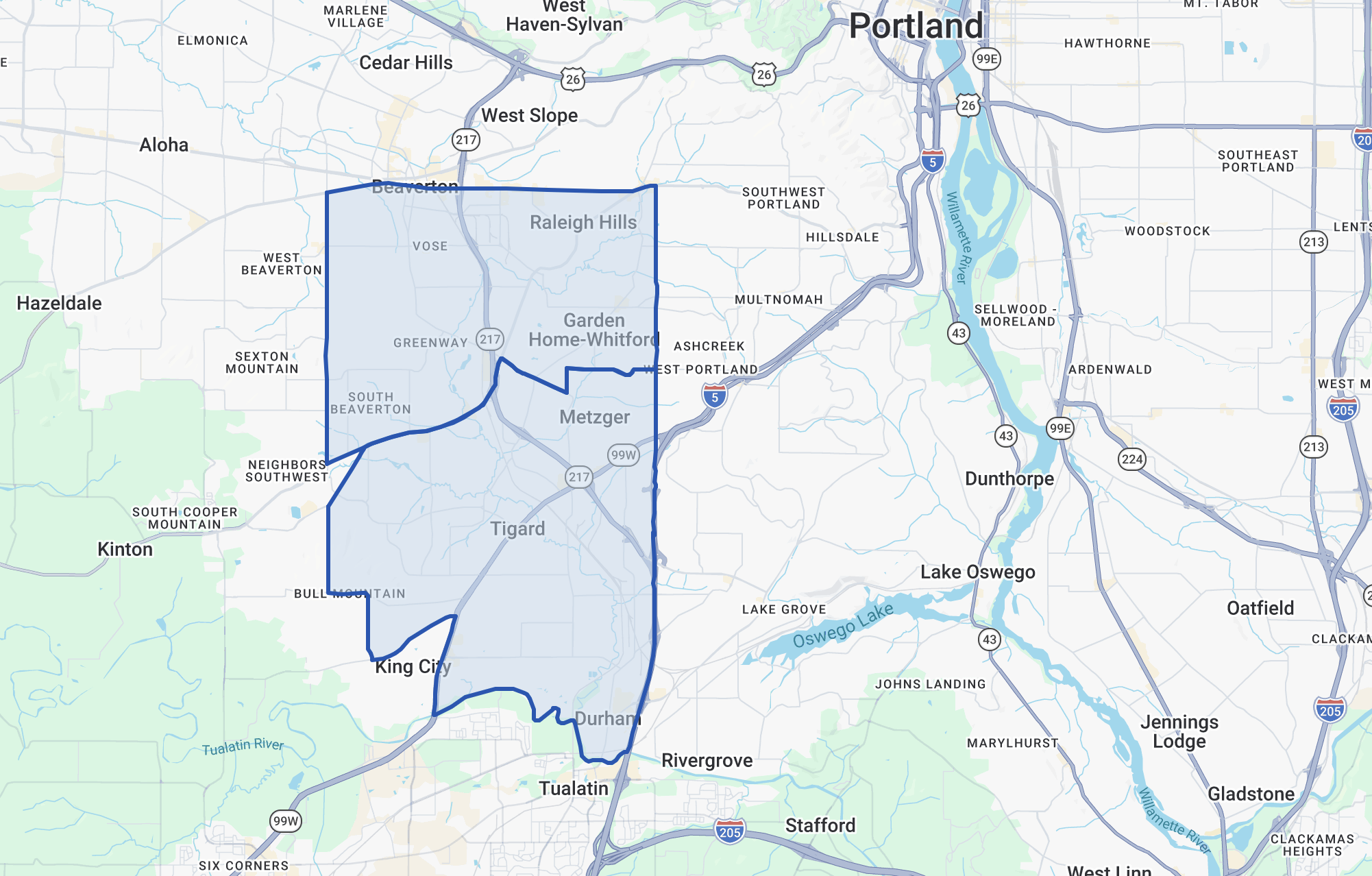

Beaverton & Tigard — 217 Corridor

Westside office market with a broad range of Class B and C product in office parks along 217, including North Beaverton and Tigard. Pricing generally runs below CBD and Kruse Way with strong parking. The submarket serves companies with westside customer bases or workforces and tenants optimizing for function and cost over prestige.

Best for: professional services, medical, engineering, insurance, and back-office users prioritizing westside access and value.

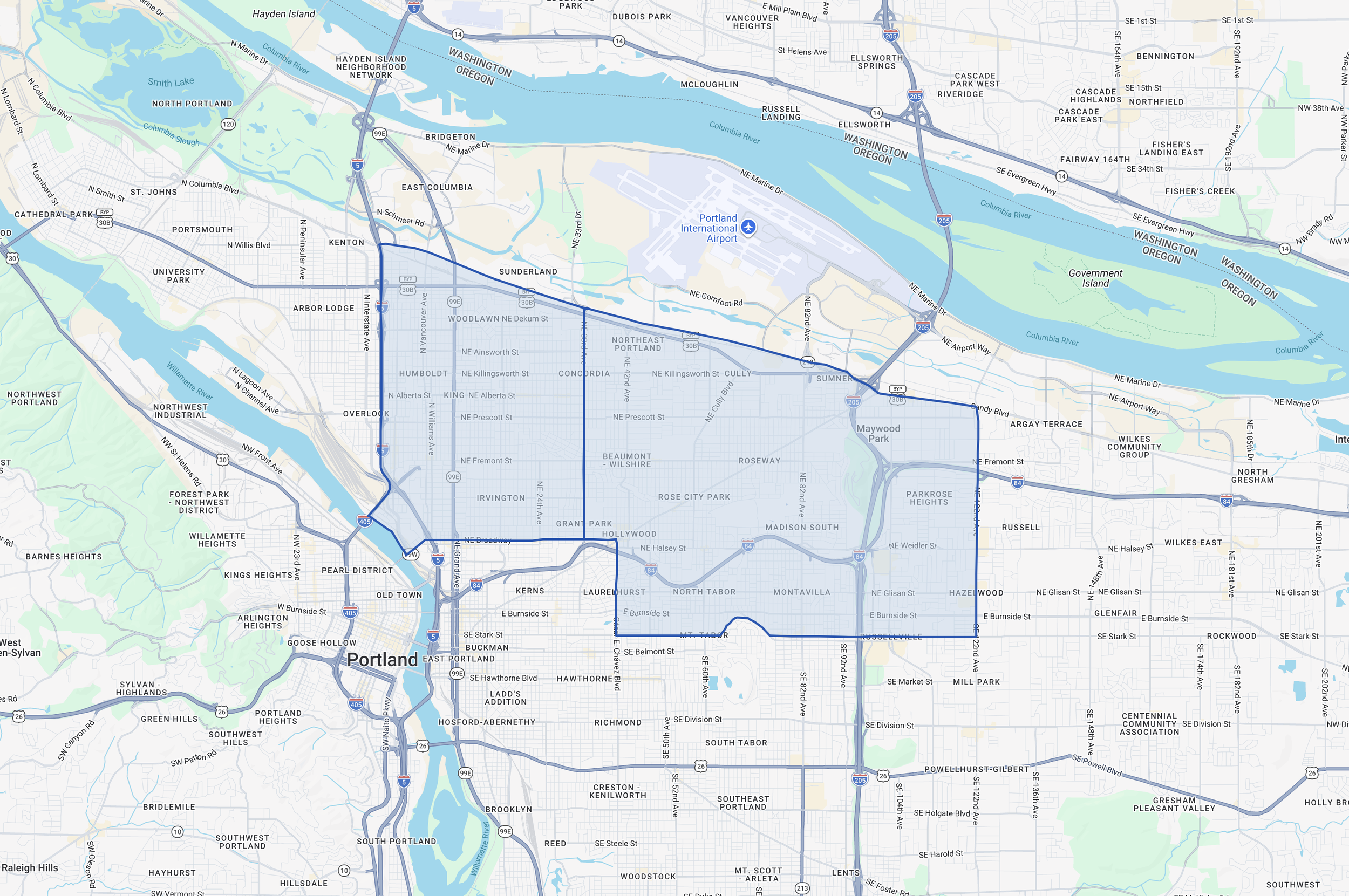

Gateway & NE Close-In

Diverse east-side office pocket spanning close-in NE Portland through the Gateway and Mall 205 areas. Inventory ranges from smaller neighborhood office product in close-in NE to larger suburban-style buildings near the Gateway transit center and I-205 interchange. Pricing generally runs below CBD and Lloyd with functional parking. Building quality varies widely — due diligence on systems and condition matters in this submarket.

Best for: medical, professional services, nonprofit, and tenants seeking east-side access with moderate pricing and proximity to I-84 and I-205 connectivity.

Explore More →

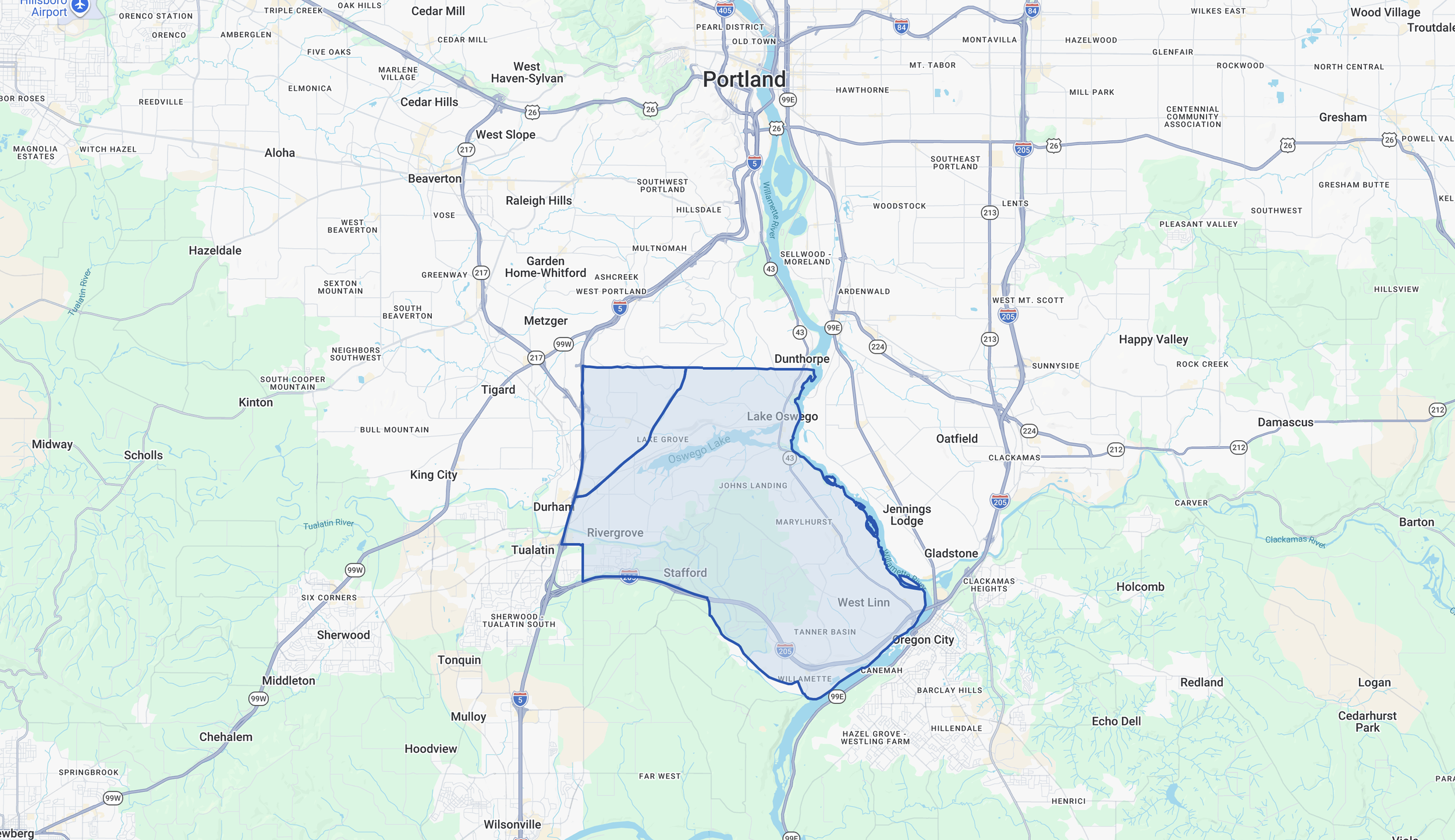

Lake Oswego & Kruse Way

Suburban Class A and B corridor south of Portland concentrated along Kruse Way, Boones Ferry, and Meadows Road. Strong parking, lower rates than CBD, and a professional tenant base weighted toward financial, legal, insurance, and medical users. Buildings tend to be lower density with parking typically included in rent.

Best for: financial services, wealth management, insurance, legal, medical office, and professional firms prioritizing suburban access and lower occupancy costs.

NEED A SHORTLIST?

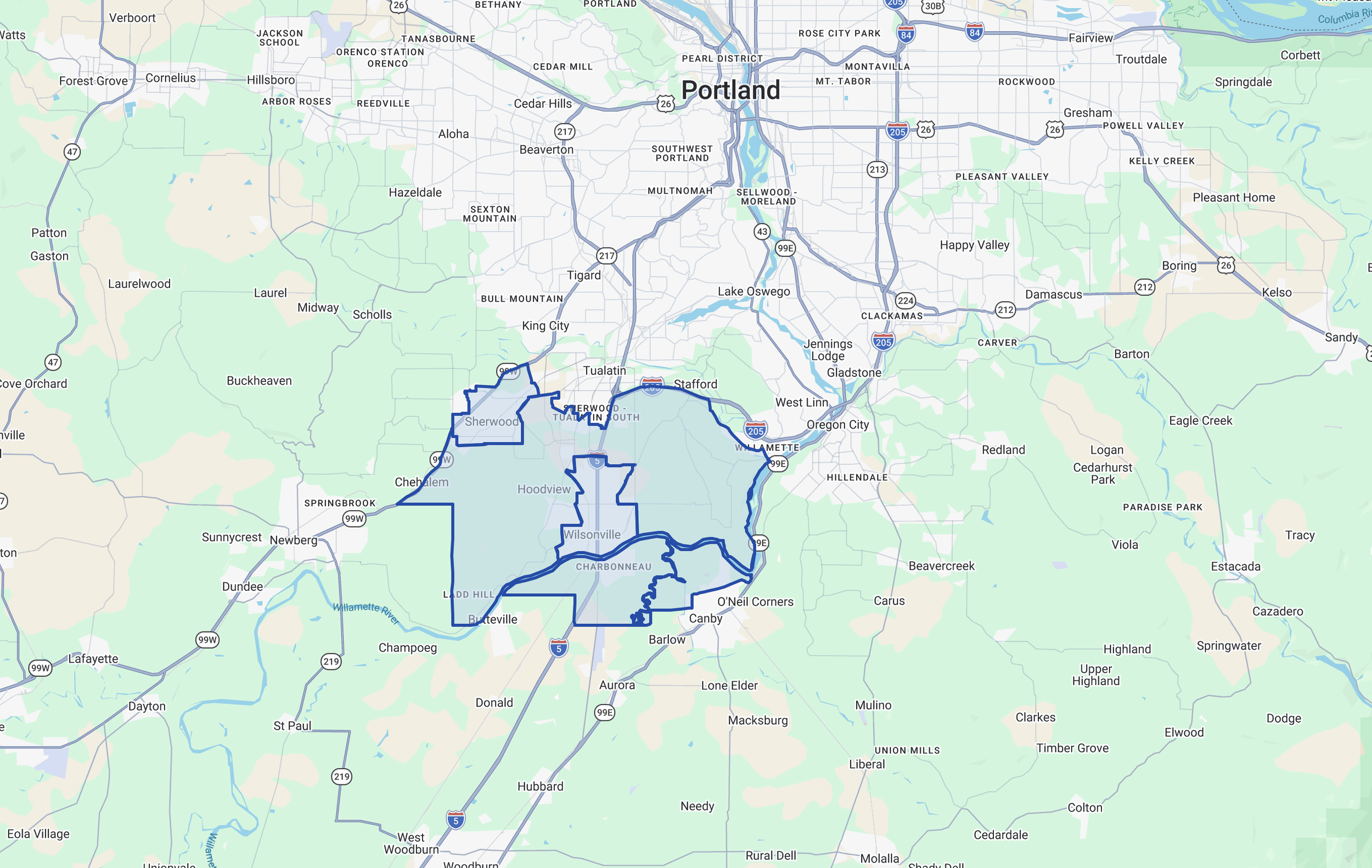

Tualatin, Wilsonville, &Sherwood

South metro office market along the I-5 and 99W corridors. Inventory is a mix of office park product and flex/office buildings, generally newer than close-in Portland options. The submarket serves companies with south metro workforces or client bases and tenants who prioritize I-5 access, functional sites, and competitive pricing over urban proximity.

Best for: professional services, engineering, medical, and companies with south metro or Salem-corridor client and employee geography.

Explore More →

Share use, size, timing, and must-haves (parking ratio, floor size, building class). Receive a realistic availability shortlist and next-step plan aligned to current market conditions.

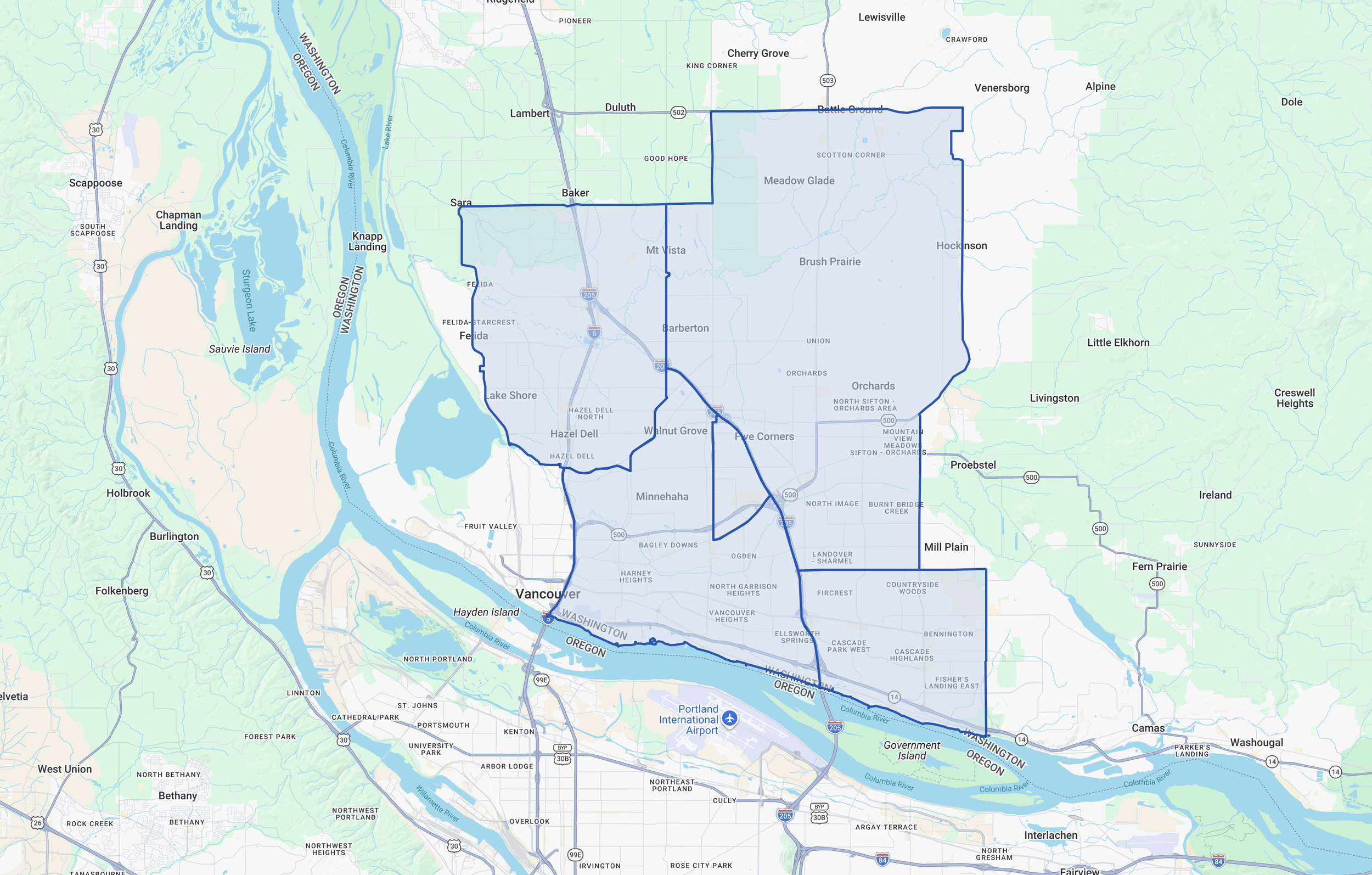

Vancouver, WA

Suburban office market spanning West Vancouver/CBD, central Vancouver, Cascade Park, Hazel Dell, and the Vancouver Waterfront. No state income tax for Washington-resident employees is a meaningful draw. Pricing generally runs below comparable Portland product with strong parking. The Waterfront has added newer institutional-quality product. Columbia River crossing congestion is a real commute factor for Oregon-side employees.

Best for: professional services, healthcare, finance, and companies with Washington-based workforces or clients seeking tax-advantaged positioning.

Explore More →

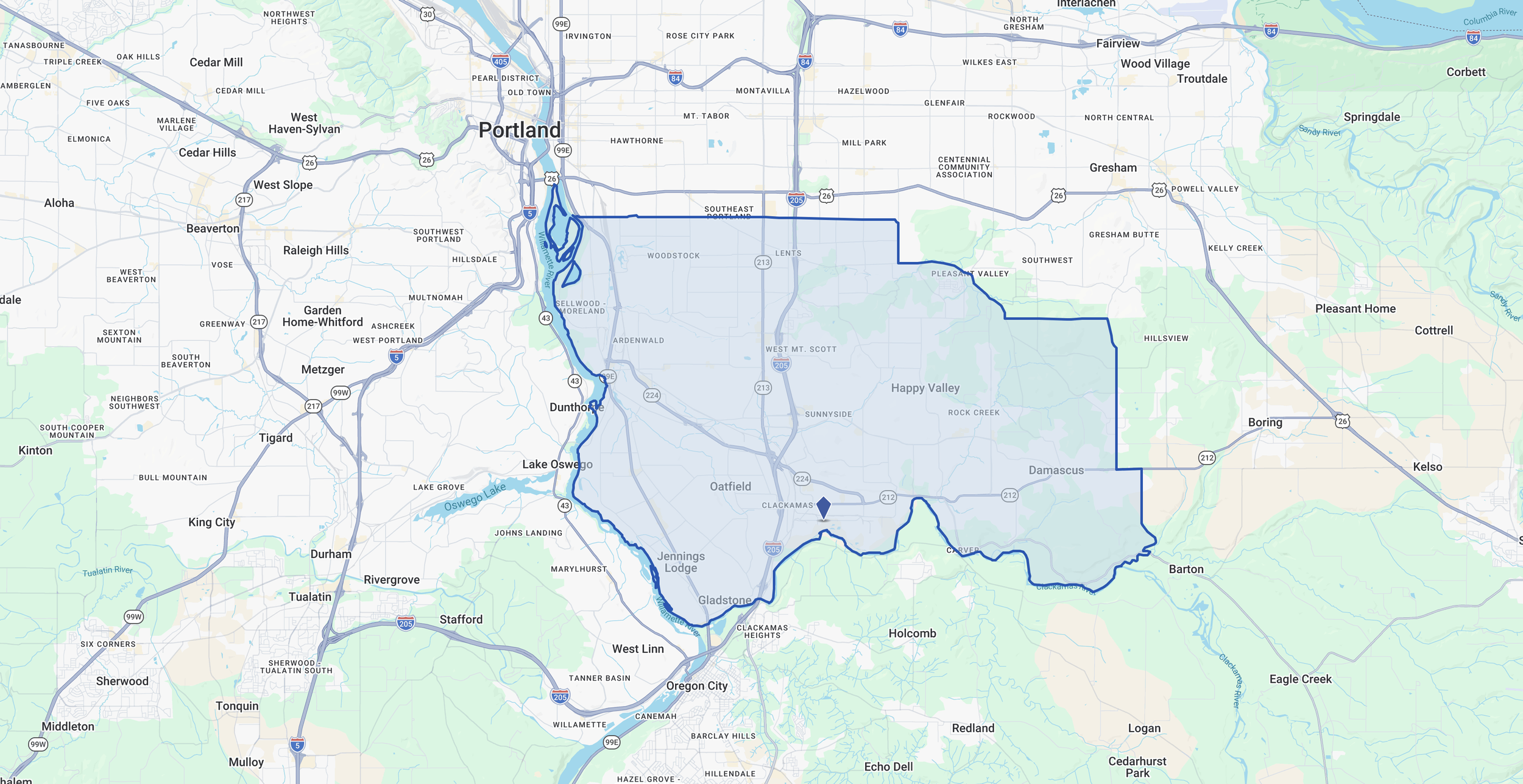

Clackamas & Milwaukie

Southeast metro office market along the I-205 and 82nd/99E corridors with a mix of Class B and C product. Pricing is value-oriented with strong parking ratios. The submarket includes Clackamas, Milwaukie, outer SE, and extends to Oregon City. Building stock varies widely in age and quality — condition and systems due diligence is important, particularly on lower-priced product.

Best for: medical, insurance, professional services, government, and tenants seeking southeast metro access with value-oriented economics.

Explore More →

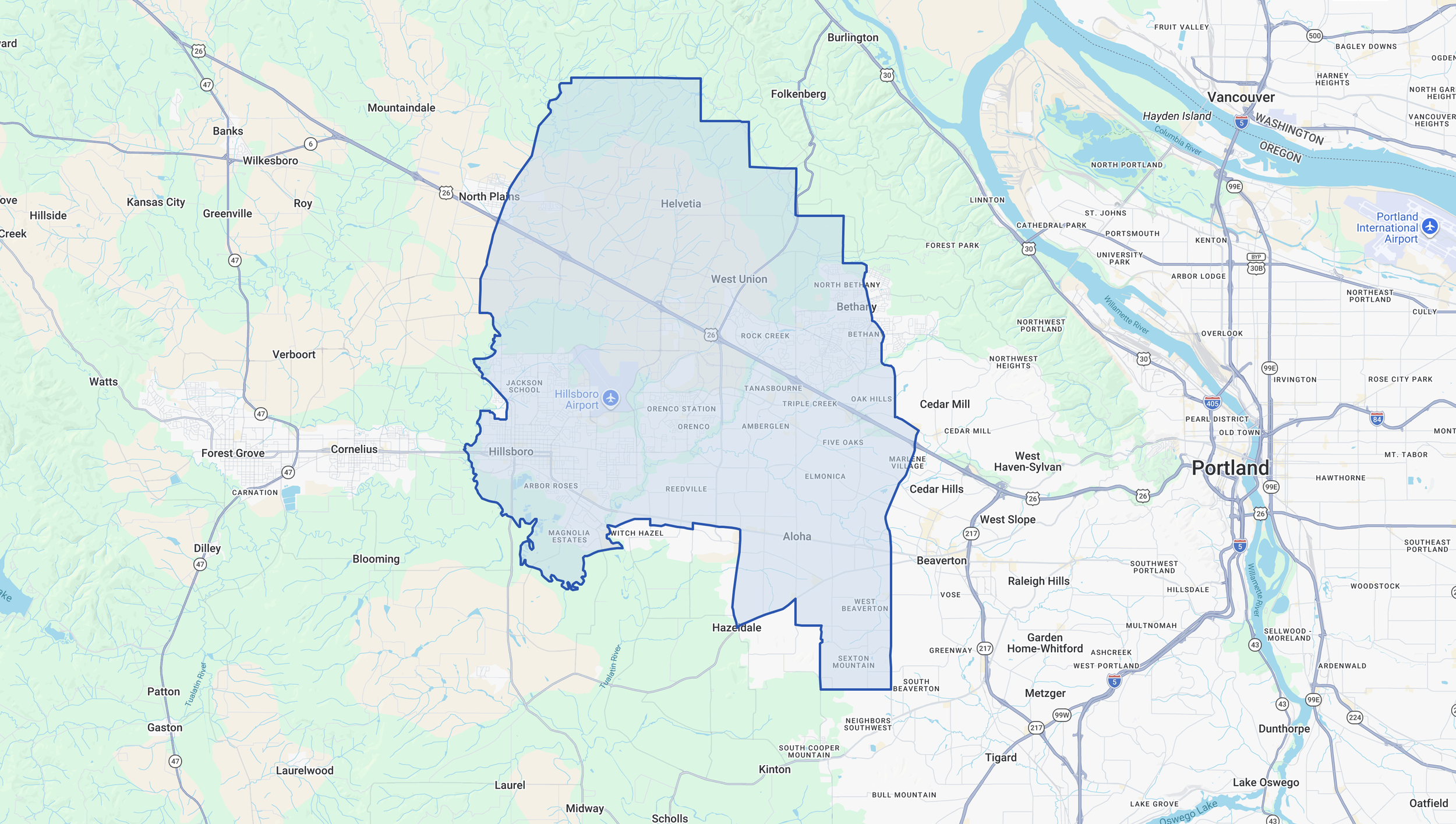

Sunset Corridor & Hillsboro

Westside office and flex market tied to the tech and semiconductor employment base along US-26. Inventory includes corporate campus product and multi-tenant office parks. Availability can swing based on corporate expansion and contraction cycles and sublease releases from larger tenants.

Best for: tech companies, engineering firms, and businesses with workforces or clients concentrated in the US-26/Hillsboro corridor.

Explore More →

COMMON QUESTIONS ABOUT PORTLAND OFFICE SUBMARKETS

-

It depends on what you're optimizing for. Downtown / CBD offers the strongest institutional presence, transit access, and central visibility — most law firms, accounting firms, and financial services companies locate here for client-facing credibility. Kruse Way / Lake Oswego provides a suburban alternative with lower occupancy costs, strong parking, and a professional tenant base. Lloyd District offers CBD-adjacent positioning at lower rates. The "best" choice usually comes down to where your clients are, where your employees live, and how much parking matters to your operation.

-

Parking is one of the biggest functional differentiators between Portland office districts. Downtown / CBD typically offers 0.5 to 1.5 spaces per 1,000 SF, often in structured garages at additional cost. Pearl District is similar or tighter, with most parking priced separately. Suburban markets (Kruse Way, 217 Corridor, Vancouver) generally offer 3.0 to 4.5 spaces per 1,000 SF, typically included in rent through surface lots or structured parking. Lloyd falls in between at roughly 2.0 to 3.5 per 1,000 SF. For tenants whose employees drive, parking economics can shift the effective cost comparison between submarkets significantly.

-

Elevated vacancy across most Portland office submarkets — particularly in CBD and Class B suburban product — has created meaningful concession packages. Landlords are offering free rent periods, increased TI allowances, reduced escalation schedules, and flexible early termination options that weren't available three years ago. The gap between asking rent and effective rent (after concessions are factored in) can be significant, especially for creditworthy tenants willing to commit to longer terms. Comparing spaces on asking rate alone without accounting for concessions and total occupancy cost produces misleading economics.

-

Start 9–12 months before expiration for most office tenants, earlier if you're above 10,000 SF or need significant buildout. Even if you expect to renew, running a parallel relocation search creates leverage that directly affects renewal economics — landlords negotiate more aggressively when they know the tenant has real alternatives. Waiting until the final few months eliminates options, weakens your negotiating position, and often results in accepting the landlord's initial proposal with minimal improvement.

-

Office leases use several expense structures, and comparing them requires normalization. Full-service gross bundles operating expenses into the base rent with escalations tied to expense increases over a base year. Modified gross typically passes through some but not all expenses. NNN passes through taxes, insurance, and operating expenses directly. Two buildings with the same base rent can have meaningfully different total occupancy costs depending on expense structure, base year, gross-up provisions, and what's included or excluded. Always compare on total occupancy cost per SF including estimated expenses, parking, TI amortization, and concession credits — not just asking rate.

-

Building class is an informal designation reflecting quality, age, amenities, and location. Class A buildings are typically newer or recently renovated, institutionally owned, and offer the strongest finishes, lobby presence, building systems, and common-area amenities. Class B buildings are functional and well-maintained but may lack the finishes, systems, or common areas of Class A. Class C is older product, often with deferred maintenance and limited amenities. In Portland's current market, the distinction matters because flight to quality is real — tenants are upgrading from B to A space when concession packages make it economically feasible, which is compressing Class A effective rates while leaving some Class B product with persistent vacancy.

-

Sublease space has been a significant factor in Portland's office market since 2020. Sublease listings can offer below-market rates, existing buildouts, and shorter term commitments that appeal to tenants who need flexibility or want to test a location before committing to a direct lease. However, sublease space comes with limitations: the term is fixed to the master lease expiration, renewal rights are typically unavailable, TI options are limited to what's already built, and the subtenant's rights are subordinate to the master lease. In some cases, sublease options create competitive pressure on direct landlords, which can benefit tenants negotiating direct leases in the same building or submarket.

GET IN TOUCH

Contact Matt Lyman at Norris & Stevens about leasing, renewing, or relocating office space in Portland — whether you're evaluating submarkets, comparing available options, or need a market opinion on your current lease.

Share your space requirements — size range, parking needs, building class preferences, location priorities, and timeline — and Matt will follow up with current availability, recent lease comps, and a recommended approach.

Coverage spans the Portland metro office market — Downtown/CBD, Pearl District, Lloyd District, Central Eastside, Lake Oswego/Kruse Way, 217 Corridor/Beaverton/Tigard, Johns Landing/Macadam, and Vancouver, WA.